Renault Winery Resort and Vineyard National Golf Course, Egg Harbor City, NJ — owned by Accountable Equity and operated by Vivamee Hospitality. A destination hospitality and golf complex offering multiple revenue streams — lodging, dining, events, and golf — available to accredited investors as a private investment opportunity.

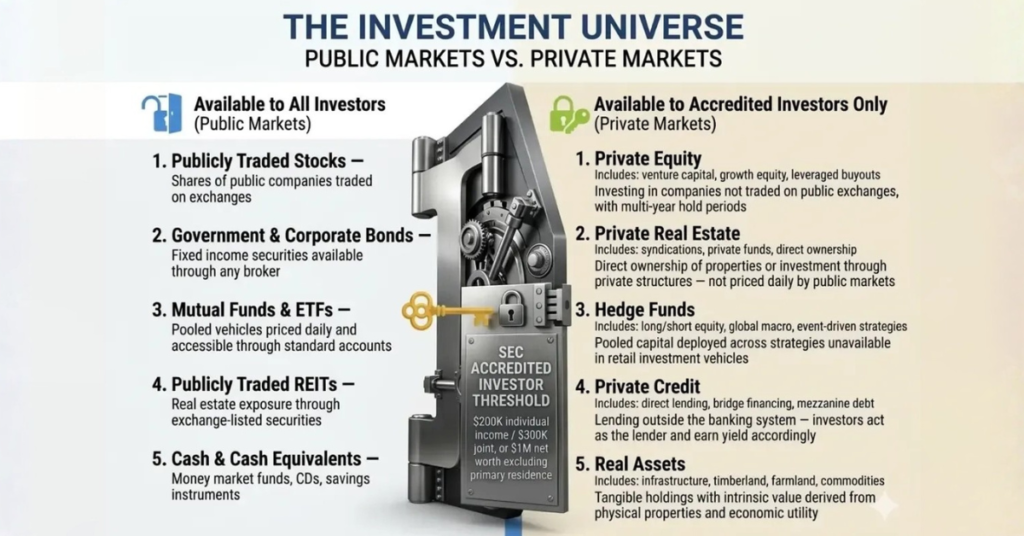

Accredited investor status opens a door. On one side is the investment universe available to virtually everyone: publicly traded stocks, bonds, mutual funds, and ETFs. On the other side is a much broader world — private equity, private real estate, hedge funds, private credit, and real assets — categories that do not trade on any exchange and are not accessible through a standard brokerage account.

The short answer: accredited investors can participate in private securities offerings that are legally unavailable to the general public. These include private real estate, private equity, hedge funds, private credit, and real assets — categories that do not trade on any exchange and are not registered with the SEC. The longer answer involves understanding why that access exists, what it actually means for your portfolio, and what separates the opportunities worth pursuing from the ones to avoid.

This post is written for investors who are new to the concept of accredited status — people who have built wealth primarily through public markets and are beginning to ask whether a different category of investment deserves a place in their portfolio. No investment is right for everyone, and this article does not constitute investment advice. Every investor should complete their own due diligence and consult with qualified professionals before making any investment decision.

In This Article

1. Why Accredited Investor Status Creates a Legal Divide

2. The Investment Categories Unlocked by Accreditation

3. Private Real Estate Syndications: What the Structure Actually Looks Like

4. What Accreditation Does Not Guarantee

5. How to Evaluate Whether You Qualify

6. Frequently Asked Questions

Why Accredited Investor Status Creates a Legal Divide

The distinction between accredited and non-accredited investors is not about sophistication in a general sense. It is a regulatory construct created by the SEC under Regulation D to determine who may legally participate in unregistered private securities offerings.

When a company registers a securities offering with the SEC — an IPO, for example — it undergoes extensive disclosure requirements designed to protect investors who may lack the financial resources or expertise to evaluate complex deals on their own. The registration process is time-consuming and expensive, but it results in a public offering that any investor can access.

Private placements bypass that registration process. They are offered under Regulation D exemptions, most commonly Rule 506(b) or Rule 506(c), and they are restricted to investors who meet certain financial thresholds. The regulatory theory is that investors above those thresholds can bear financial risk and fend for themselves without the full protection of SEC registration.

This creates a legal divide: accredited investors can participate in deals that unregistered, non-accredited investors cannot access. That divide is not a guarantee of quality. There are excellent private offerings and poor ones. The accredited investor framework simply determines who is legally eligible to be in the room.

Key Regulatory Context

Rule 506(b) offerings allow up to 35 non-accredited but sophisticated investors and do not permit general solicitation. Most private placements operate under this structure.

Rule 506(c) offerings permit general solicitation — meaning sponsors can publicly advertise the opportunity — but all investors must be verified as accredited. Accountable Equity conducts all offerings exclusively under Rule 506(c).

The Investment Categories Unlocked by Accreditation

Accredited status does not unlock a single asset type. It opens access to an entire tier of private markets that includes five major categories of investment — the same framework used by institutional portfolio managers when evaluating alternatives allocations.

Private Equity

Private equity involves investing in companies that are not publicly traded. This includes venture capital (early-stage companies), growth equity (scaling companies), and buyouts (acquiring and restructuring mature businesses). Private equity funds are structured as limited partnerships with defined hold periods — typically five to ten years — and target returns that reflect the illiquidity and complexity investors accept relative to public equity exposure.

Private Real Estate

Private real estate encompasses direct ownership of properties or investment through private funds and syndications. Unlike publicly traded REITs, private real estate is not priced daily — valuations reflect the underlying property and its cash flows, not market sentiment. Investments range from multifamily apartment complexes and industrial warehouses to specialized categories like hospitality, mixed-use development, and destination assets.

Private real estate syndications are one of the most common entry points for accredited investors new to private markets. They pool capital from multiple investors to acquire and operate properties that would be beyond the reach of individual capital — combining real asset ownership with the ability to participate at institutional scale. Section 3 of this post covers how that structure works in detail.

Hedge Funds

Hedge funds pool capital from accredited and institutional investors and deploy it across a wide range of strategies — long/short equity, global macro, event-driven, quantitative, and others — using leverage, derivatives, and concentrated positions that would not be available in a retail investment vehicle. Unlike mutual funds, hedge funds face fewer regulatory constraints on strategy and fee structures. Minimum investments are typically high, and performance fees are charged in addition to management fees.

Private Credit

Private credit refers to lending outside the banking system — direct loans to businesses, real estate bridge financing, mezzanine debt, and similar instruments. Private credit has grown significantly as banks have tightened their balance sheets, creating opportunities for private investors to act as lenders and earn yield that reflects the credit risk and illiquidity they accept. For investors seeking income-oriented alternatives, private credit can occupy a distinct role in a portfolio that neither public bonds nor equity can replicate.

Real Assets

Real assets include physical commodities, infrastructure, timberland, farmland, and other tangible holdings with intrinsic value derived from their physical properties and economic utility. Real estate is often classified separately from other real assets, though both share the tangibility characteristic that many investors find appealing as an inflation hedge. Infrastructure and farmland in particular have attracted institutional capital seeking long-duration, inflation-sensitive cash flows that are largely independent of public market cycles.

The investment universe available to accredited investors extends well beyond public markets. Private equity, private real estate, hedge funds, private credit, and real assets are each inaccessible through a standard brokerage account — and each carries a distinct return driver, risk profile, and liquidity structure.

Private Real Estate Syndications: What the Structure Actually Looks Like

For many accredited investors exploring private markets for the first time, real estate syndications represent one of the most approachable entry points. The structure is well-established, the underlying asset class is tangible, and the income mechanics are relatively transparent.

Understanding the structure is essential before evaluating any specific deal.

The General Partner / Limited Partner Structure

In a typical syndication, the general partner (GP) is the sponsoring firm. The GP identifies the deal, raises capital, executes the business plan, manages the asset, and handles distributions. The limited partners (LPs) are the passive investors. LPs contribute capital and receive returns, but they do not participate in day-to-day management decisions and are not personally liable for the debts of the partnership beyond their invested capital.

This GP/LP structure is the backbone of most private real estate investments. It allows investors to access institutional-quality deals without taking on the operational burden of direct property ownership.

How Returns Are Structured

Most real estate syndications include a preferred return — a hurdle rate that limited partners receive before the general partner participates in profits. Common structures include preferred returns in the range of 6% to 8% annualized, though the specific terms vary by deal and sponsor.

Once the preferred return is met, remaining profits are split between the GP and LPs according to a waterfall distribution schedule. For example, a common structure might allocate 70% to LPs and 30% to the GP after the preferred return threshold is reached. The specific waterfall terms are defined in the offering documents and should be reviewed carefully.

Important: These are Target Figures, Not Guarantees

Preferred return targets and projected waterfall splits are illustrative of deal structure — they are not guarantees. Real estate investments involve risk, including the potential loss of principal. Actual returns depend on property performance, market conditions, and operator execution. Past performance in any deal is not indicative of future results. Consult with a qualified financial advisor before making any investment decision

Illiquidity Is a Feature of the Structure

Private real estate syndications are not liquid investments. Capital is typically committed for a defined hold period — often three to seven years — and investors generally cannot redeem or transfer their interest freely during that period. This illiquidity is a structural characteristic of the asset class, not a flaw. It exists because the underlying assets require time to execute a business plan and realize value.

Investors evaluating private real estate should assess their overall liquidity needs carefully before committing capital to any offering. Capital committed to a syndication should be capital the investor can afford to hold for the duration of the investment period without needing to access it.

The Accountable Equity Structure

Accountable Equity raises capital through Regulation D Rule 506(c) private placement offerings and uses that capital to own destination hospitality assets — resort properties that generate revenue through lodging, events, food and beverage, and recreational programming. The properties are operated by Vivamee Hospitality, a separate operating company. Both entities were co-founded by Josh McCallen and Melanie McCallen, and Josh McCallen serves as CEO and Co-Founder of both Accountable Equity and Vivamee Hospitality.

This vertical integration between the ownership entity (Accountable Equity) and the operating entity (Vivamee Hospitality) under unified leadership is a structural differentiator. Most real estate syndications contract with third-party managers, creating a separation between the investor’s returns and the operator’s incentives. AE’s model aligns both.

What Accreditation Does Not Guarantee

Accredited investor status unlocks access. It does not confer any protection from bad deals, poor operators, or market risk. This distinction matters enormously.

The SEC’s rationale for the accredited investor framework is that investors above the financial thresholds can absorb losses without catastrophic consequences and can evaluate opportunities without the full registration and disclosure protections afforded to retail investors. That is a financial capacity assumption, not a judgment about the quality of any specific offering.

The most common misconceptions accredited investors carry into private markets include:

- Assuming regulatory approval: A Regulation D exemption means the offering is exempt from SEC registration — it does not mean the SEC has reviewed or approved the investment. No federal or state regulator has validated the quality of the deal.

- Treating preferred returns as fixed income: A preferred return in a real estate syndication is a target return structure, not a bond-like obligation. If the property underperforms, distributions may be delayed, reduced, or suspended.

- Conflating track record with future performance: A sponsor’s historical returns are relevant context but they are not predictive. Real estate markets, capital markets, and execution quality all vary. Past performance is not indicative of future results.

- Ignoring the importance of operator quality: In private real estate, the sponsor — the general partner — is as important as the asset. A well-located property managed by an inexperienced or misaligned operator can underperform. Due diligence on the sponsor matters as much as due diligence on the deal.

Understanding these limitations is not a reason to avoid private markets. It is the foundation for evaluating them correctly.

How to Evaluate Whether You Qualify

Accredited investor status under SEC Rule 501(a) can be established through financial thresholds or through professional credentials. The most common qualification paths are income-based and net worth-based.

Income-Based Qualification

An individual qualifies based on income if they have earned more than $200,000 in each of the two most recent calendar years (or more than $300,000 combined with a spouse or spousal equivalent) and reasonably expect to reach the same threshold in the current year. Both years must individually exceed the threshold — a single qualifying year is not sufficient.

Income for this purpose generally includes wages, business earnings, capital gains, rental income, and other sources. The income calculation methodology is not fixed by SEC rule, and how certain income items are treated can vary. Your CPA is the best resource for confirming how your income qualifies for accredited investor purposes in connection with any specific offering.

Net Worth-Based Qualification

An individual also qualifies if their net worth — or their joint net worth with a spouse or spousal equivalent — exceeds $1 million, excluding the value of their primary residence. As of 2010, the primary residence is excluded from both the asset and liability sides of the calculation, with one exception: if the mortgage on the primary residence exceeds the home’s fair market value, that excess is counted as a liability.

Professional Credential Qualification

Individuals holding certain FINRA licenses — specifically Series 7, Series 65, or Series 82 in good standing — qualify as accredited investors based on professional credentials rather than financial thresholds. This pathway acknowledges demonstrated financial sophistication independent of personal wealth.

In a 506(c) offering such as those conducted by Accountable Equity, the sponsor must take reasonable steps to verify that each investor meets accredited investor criteria. Verification is typically accomplished through third-party letters from CPAs, attorneys, or broker-dealers, or through financial documentation review. Investor self-certification alone is not sufficient under Rule 506(c).

Frequently Asked Questions

Do I need to prove my accredited investor status every time I invest?

It depends on the offering structure. In a 506(b) offering, the sponsor must have a reasonable basis to believe you qualify — typically established through a questionnaire or subscription agreement. In a 506(c) offering, active verification is required by the issuer. Third-party verification letters from CPAs, attorneys, or broker-dealers are commonly used. There is no fixed regulatory standard for how long a verification letter remains valid. Timing requirements vary by offering and sponsor — confirm the specific requirements with each offering before relying on an existing letter.

Can I access these investments through my IRA or retirement account?

In some cases, yes. A self-directed IRA can hold certain alternative investments, including real estate syndication interests, provided the custodian and the offering permit it. The rules governing self-directed IRAs are complex, including restrictions on self-dealing and prohibited transactions. Investors interested in using retirement funds for private placements should consult with a qualified tax and financial advisor before proceeding.

Is there a public database of legitimate accredited investor offerings?

No. Private placements are not required to be listed in any central public registry. Investors typically access offerings through sponsor relationships, registered investment advisers, broker-dealers, or accredited investor networks. Because there is no central registry, the quality of deal flow is heavily dependent on the relationships and diligence an investor builds over time.

What is the minimum investment typically required for a private real estate syndication?

Minimums vary widely by offering and sponsor. Entry points can range from $25,000 for some fund structures to $100,000 or more for direct deal co-investments. The minimum is set by the sponsor and defined in the offering documents. Investors should evaluate whether the minimum creates appropriate diversification across their overall alternative investment allocation.

How do I evaluate a sponsor before investing?

Sponsor evaluation is one of the most important skills in private investing. Key areas to examine include track record across multiple market cycles, the alignment between ownership and operations, fee structures relative to industry norms, how distributions have been handled in prior deals, and the clarity and transparency of investor communications. The upcoming post in this series on due diligence and sponsor evaluation covers this in detail.

Conclusion

Accredited investor status creates legal access to an investment tier that most market participants will never see. That access includes private equity, private real estate, hedge funds, private credit, and real assets — categories that have historically offered diversification, income, and return profiles not available through a standard brokerage account.

Access, however, is not the same as outcome. The quality of private market returns depends on operator quality, deal structure, market conditions, and the discipline of the investor’s evaluation process. Understanding what the door opens — and what it does not guarantee — is the starting point for using that access well.

If you are an accredited investor exploring private real estate for the first time, the most important next step is building your evaluation framework before you commit capital. Future posts in this series cover sponsor due diligence, deal structure mechanics, and how to think about private real estate as part of a broader portfolio.

UP NEXT IN THIS SERIES

Why Wealthy Investors Limit Their Stock Market Exposure

Now that you understand what accredited status unlocks, the next post examines why many high-net-worth investors deliberately reduce their public market exposure — and what they allocate to instead.