Wealthy investors limit stock market exposure not because they have abandoned equities, but because they have recognized a flaw in the conventional diversification model that most investors never question. The standard 60/40 portfolio — 60% stocks, 40% bonds — was designed so that bonds would cushion equity losses during downturns. For decades, that assumption held. Then 2022 arrived, and both stocks and bonds declined simultaneously. The 60/40 investor had nowhere to hide.

That single year exposed what institutional investors had understood for much longer: the real diversification problem is not how much you hold in stocks. It is whether your non-stock positions are actually uncorrelated — or just feel that way. Bonds and stocks failed together because they shared a common enemy: rising interest rates. True diversification requires assets whose returns are driven by fundamentally different forces entirely.

This post explains why the correlation problem matters, what sophisticated investors hold instead, and how accredited investors can access the same alternatives that institutions and family offices have used for decades to manage this risk.

The traditional 60/40 portfolio assumes stocks and bonds move independently. In 2022, both declined simultaneously. Investment opportunities in uncorrelated real assets like those owned by Accountable Equity and operated by Vivamee Hospitality are available exclusively to accredited investors.

TABLE OF CONTENTS

1. The Problem with the 60/40 Portfolio

2. Correlation: Why “Diversified” Portfolios Often Are Not

3. What Do Real Assets Offer Instead?

4. How Accredited Investors Access These Alternatives

5. The Shift Is Already Happening

FAQ

Conclusion

The Problem with the 60/40 Portfolio

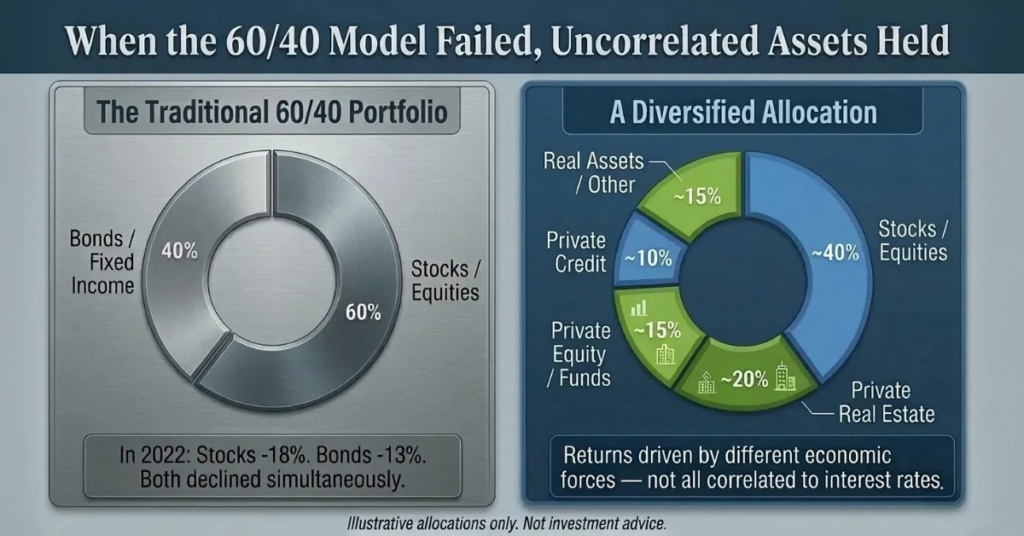

The 60/40 portfolio — 60% stocks, 40% bonds — became the dominant model for balanced investors because it worked. For most of the past 40 years, when equities fell, bonds rallied. The negative correlation between the two asset classes meant that a portfolio split between them smoothed out volatility and protected investors from the worst of equity drawdowns.

Then in 2022, the Federal Reserve began one of the most aggressive interest rate hiking cycles in modern history. Both stocks and bonds fell sharply — and simultaneously. According to Bloomberg index data, the U.S. Aggregate Bond Index dropped more than 13% for the year — its worst annual performance on record. According to S&P Dow Jones Indices data, the S&P 500 declined more than 18% over the same period. The result, widely reported by financial analysts, was the worst calendar year for the 60/40 portfolio in decades.

What 2022 demonstrated was not a one-time anomaly. It was a structural vulnerability that had always existed but had been masked by four decades of falling interest rates. The 60/40 model assumes stocks and bonds are uncorrelated. They are not — they share a common sensitivity to the interest rate environment. When that shared sensitivity becomes the dominant market force, both positions decline at the same time for the same reason.

Sophisticated investors had understood this for years, which is why institutional portfolios — university endowments, pension funds, sovereign wealth funds — had long held significant allocations to private real estate, private equity, and real assets alongside their public market positions. The goal was never to exit stocks. It was to hold assets whose returns are driven by fundamentally different economic forces.

Correlation: Why “Diversified” Portfolios Often Are Not

Correlation measures how closely two investments move in relation to each other. A correlation of 1.0 means two assets move in perfect lockstep. A correlation near zero means their movements are largely unrelated. Negative correlation means they tend to move in opposite directions — the condition the 60/40 model relied upon.

The challenge for investors building portfolios from publicly traded securities is that correlation among public assets tends to increase precisely when it matters most — during market stress. In normal conditions, different stock sectors, international equities, and bonds may behave somewhat independently. During broad market selloffs, correlations converge. Everything goes down together because the same investors are selling everything at the same time for the same reasons.

Private real estate sidesteps this dynamic because it does not trade on public markets. A resort property generating revenue from room bookings, weddings, and food and beverage operations does not re-price daily based on investor sentiment. Its value is derived from physical occupancy, operating performance, and property appreciation — none of which are directly determined by what the Nasdaq does on a given Tuesday

Why This Matters More as Wealth Grows

The stakes of correlation risk increase with portfolio size. An investor with $150,000 in a brokerage account can absorb a 30% drawdown and recover over time. An investor with $3,000,000 in a portfolio that drops 30% has lost $900,000 — a figure that represents years of compounding, and one that is increasingly difficult to recover as retirement horizons shorten.

This is why high-net-worth investors consistently move toward lower-correlation assets as portfolios grow. It is not pessimism about public markets. It is precision about what risks are worth accepting at what stage of wealth accumulation — and a recognition that the 60/40 model, however elegant in theory, does not solve the correlation problem that matters most.

What Do Real Assets Offer Instead?

The term “real assets” refers to physical assets — real estate, infrastructure, commodities, and in some structures, operating businesses tied to tangible property. They are distinct from “paper assets” like stocks and bonds, which represent claims on financial performance rather than ownership of something physical.

Real assets offer several characteristics that make them attractive complements to a stock-heavy portfolio:

- Income generation independent of public markets. A well-operated real estate asset produces rental income, event revenue, or hospitality revenue regardless of what the S&P 500 does. That income stream is driven by occupancy, pricing, and operating execution — not market sentiment.

- Appreciation tied to physical scarcity. Real property appreciates when demand for that location or asset type increases. That appreciation does not reverse because a tech stock reported a disappointing quarter.

- Inflation sensitivity. Real assets historically maintain or increase their value during inflationary periods, because the replacement cost of physical assets rises with inflation. Stocks do not offer this protection consistently.

- Structural cash flow predictability. In real estate syndications, investors receive targeted distributions on a regular schedule — typically annually — based on the operating performance of the underlying asset. This is structurally different from stock dividends, which can be cut at any time.

Kent Island Resort, Chester, MD — a waterfront destination hospitality asset on Thompson Creek owned by Accountable Equity and operated by Vivamee Hospitality. Real assets like this offer returns driven by operating performance, not stock market sentiment.

Destination hospitality assets offer a specific form of this thesis. A property like Kent Island Resort — a waterfront boutique resort on Thompson Creek, which leads to the Chesapeake Bay, owned by Accountable Equity and operated by Vivamee Hospitality — generates revenue across multiple streams: room bookings, dining, and events. That operational diversification within a single asset provides income stability that a single-tenant commercial real estate investment cannot.

Josh McCallen, CEO and Co-Founder of both Accountable Equity and Vivamee Hospitality, has built the investment thesis around exactly this model: owning destination hospitality assets where the operating company — Vivamee Hospitality — is positioned to drive performance across multiple revenue channels, not just seasonal room revenue. Investors can learn more about how Accountable Equity structures its offerings at accountableequity.com/fund/.

How Accredited Investors Access These Alternatives

The investments that institutional portfolios rely on to manage correlation risk — private real estate, private equity, private credit, and real assets — are largely inaccessible to the general public. They are offered under securities regulations that restrict participation to accredited investors as defined by applicable securities laws.

An accredited investor, under current SEC definition, is an individual with annual income exceeding $200,000 (or $300,000 jointly with a spouse or domestic partner in each of the last two years with expectation of the same), or a net worth exceeding $1,000,000 excluding primary residence. This threshold exists because private placement investments carry risks and illiquidity profiles that require investors to be in a financial position to absorb them.

Accountable Equity conducts all offerings exclusively under Regulation D Rule 506(c) — which permits general solicitation but requires active verification of accredited investor status. Self-certification is not sufficient. Verification must be completed through a qualified third party or via acceptable documentation before an investor can participate.

Once verified, accredited investors can access real estate syndications — pooled investment vehicles where a general partner (GP) acquires and operates an asset on behalf of limited partners (LPs). The LPs provide equity capital and receive a targeted preferred return before the GP participates in profits. This structure aligns the interests of the operating partner with the investors in a way that stock ownership simply cannot replicate.

The Shift Is Already Happening Among Sophisticated Investors

This is not a theoretical reallocation. According to data from Preqin, a leading alternative assets research firm, institutional investors globally have steadily increased their allocations to private markets over the past two decades — with private real estate, private equity, and infrastructure now representing a substantial share of endowment and pension fund portfolios. The Yale University Endowment, widely studied as a model for institutional asset allocation, has maintained alternative asset allocations exceeding 70% of its portfolio for years, with private real estate and real assets among its core holdings. These are not fringe allocations — they reflect a deliberate, long-term structural decision by the most sophisticated capital allocators in the world.

The difference between institutional investors and accredited individuals has historically been access. Institutions have always had the scale, legal infrastructure, and minimum investment capacity to participate in private placements. That same access is now available to accredited individuals — but most are not yet using it.

The gap between institutional and individual accredited investor behavior is measurable. According to the SEC’s Office of the Investor Advocate, based on January 2024 survey data, only approximately 4.3% of accredited investors currently own private-market securities — despite qualifying to do so. A 2025 Goldman Sachs Asset Management survey of investors with over $1 million in investable assets found that alternatives adoption rises sharply with wealth: 39% of households with $1–5 million utilize alternatives, a figure that climbs to 63% for those with $5–10 million and 80% for those with over $10 million. The pattern is clear — as capital grows, sophisticated investors move toward uncorrelated assets. Most accredited investors at the lower end of the wealth spectrum have not yet made that shift.

Accountable Equity invests in destination hospitality assets that generate this kind of operating-backed return. The portfolio — which includes Renault Winery Resort, Kent Island Resort, LBI National Golf and Resort, and Bohemia Manor Farm — is designed to produce performance that is not correlated to public market movements. Each property is operated by Vivamee Hospitality; explore the portfolio at vivamee.com.

Frequently Asked Questions

Doesn’t the 60/40 portfolio already solve the diversification problem?

The 60/40 model was built on the assumption that stocks and bonds are negatively correlated — that when equities fall, bonds rally. That assumption held for most of the past four decades because interest rates were generally declining. In 2022, when the Fed raised rates aggressively to combat inflation, both stocks and bonds declined simultaneously, and the 60/40 portfolio delivered its worst year in decades. The model does not solve the correlation problem; it papers over it under specific rate conditions. True diversification requires assets whose returns are driven by fundamentally different forces than either public equities or interest rates.

Is limiting stock market exposure only relevant for very large portfolios?

The principle applies at any level, but the regulatory access point for many of the most effective alternatives — real estate syndications, private equity funds, private credit — is the accredited investor threshold. Investors who qualify under current SEC definitions can begin building a more diversified allocation once they understand what these vehicles are and how they work.

What is the difference between investing in a real estate syndication and buying a REIT?

A REIT (Real Estate Investment Trust) is a publicly traded security that moves daily with market sentiment — even though the underlying assets are physical properties. A real estate syndication is a private placement: investors own a direct equity interest in a specific asset or portfolio, and returns are tied to that asset’s operating performance. Syndications are illiquid and require a longer hold horizon, but they offer the low correlation benefit that REITs, as public securities, cannot fully provide.

Do all accredited investors qualify for real estate syndication offerings?

Qualification depends on the specific offering structure. Accountable Equity conducts all offerings under Regulation D Rule 506(c), which requires active third-party verification of accredited investor status prior to participation. Investors who meet the income or net worth thresholds and complete the verification process are eligible to review offering materials and participate.

What is a preferred return and how does it protect investors in a syndication?

A preferred return is the minimum return that limited partner investors are targeted to receive before the general partner earns any carried interest. It functions as a priority claim on cash flow distributions: LPs receive their targeted preferred return first. Only after that threshold is met does the general partner begin participating in excess profits. This structure is designed to align GP incentives with LP performance, though it does not guarantee returns and is subject to the fund achieving its operational targets.

Conclusion

The 60/40 portfolio is not wrong — it is incomplete. It solved the right problem for a specific market environment, and for decades it worked. What 2022 demonstrated is that the diversification it provided was conditional: it depended on stocks and bonds moving independently, and when that relationship broke, investors had no uncorrelated position to absorb the loss.

Wealthy investors and institutions had already drawn this conclusion. Their response was not to abandon public markets but to complement them with assets whose returns are driven by fundamentally different forces — private real estate, operating businesses, real assets. These positions do not eliminate risk. They change which risks the portfolio is exposed to, and they reduce the likelihood that everything declines at the same time for the same reason.

Accredited investors have access to the same vehicles. Real estate syndications — particularly those backed by destination hospitality assets with multiple operating revenue streams — offer the kind of uncorrelated, income-generating exposure that institutional portfolios are built around. If you are evaluating whether alternatives belong alongside your current allocation, learn more about how Accountable Equity structures its offerings at accountableequity.com/fund/.

COMING UP NEXT :

How to Invest in Hospitality Real Estate: What Accredited Investors Need to Know

Now that you understand why sophisticated investors reduce stock market concentration, the next step is understanding one of the specific asset classes they use to do it — hospitality real estate, how it works as an investment, and what accredited investors need to evaluate before committing capital.