The funds offered by Accountable Equity own real, operating resort properties — and that tangible ownership is the prerequisite for every tax benefit described in this post.

The tax benefits of real estate syndication are real, significant, and systematically underutilized by accredited investors who built their wealth in W-2 income and public markets. Unlike a brokerage account, where your gains are taxed at sale, real estate syndication delivers tax advantages that begin working from the moment an asset is placed in service — and they compound materially across a multi-asset portfolio.

But these benefits only work if you understand the mechanics before you invest. This post explains the core tax advantages available through real estate syndication — depreciation, bonus depreciation, cost segregation, and K-1 treatment — in plain terms, with no projected savings and no promises. Every investor’s tax situation is different. What follows is education, not advice.

Who this post is for

Accredited investors who have built wealth primarily through employment income, stock market accounts, or a business sale — and who may not yet understand how real estate syndication creates tax-advantaged income. If you already know how K-1s and depreciation work, this post will serve as a useful review and confirmation that the mechanics apply to private real estate funds.

Why Real Estate Gets Special Tax Treatment

The U.S. tax code has long distinguished between active income — wages, salaries, business profits — and passive income from investments. Real estate occupies a unique position in that framework because it is a tangible, depreciable asset. The IRS allows property owners to write off the theoretical “wear and tear” on a building over time, regardless of whether the property’s market value is declining. In many cases, it isn’t.

This is the foundational insight: you can own a property that is generating income and appreciating in value, while simultaneously reporting a paper loss on your tax return due to depreciation. That paper loss can offset other income — subject to your specific tax situation and the rules governing passive activity losses.

A critical note: This dynamic applies specifically to real estate ownership. It is not available through REITs, mutual funds, or exchange-traded funds. When you own shares of a REIT, you own shares — not an interest in real property. The tax treatment is fundamentally different. In a real estate syndication structured as a private placement fund, you receive a direct ownership interest in the fund, which in turn holds real property. That ownership chain is what makes the following tax mechanics possible.

Depreciation: The Engine Behind Real Estate’s Tax Advantage

Depreciation is the annual deduction allowed for the theoretical decline in a property’s useful life. The IRS assigns a useful life of 27.5 years to residential real estate and 39 years to commercial real estate. A fund that owns a $10 million commercial property can deduct roughly $256,000 per year in depreciation — reducing taxable income by that amount before distributions are calculated.

In a fund structure, those depreciation deductions flow through to investors on a Schedule K-1, proportional to their ownership interest. The K-1 is the document you receive each year from the fund — it replaces the 1099 you’d receive from a brokerage account and reports your share of income, deductions, and other tax items.

What to expect from your K-1

A K-1 from a real estate syndication fund will typically report: your share of ordinary income or loss from operations; your share of depreciation deductions; and your share of any capital gains or losses on asset sales. The combination of income and depreciation often results in a lower taxable income figure than the cash you actually received. This is the core mechanism of real estate’s tax efficiency. Consult your CPA to understand how these items flow into your personal tax return.

Bonus Depreciation and Cost Segregation: Accelerating the Benefit

Standard depreciation is taken over 27.5 or 39 years. Two additional tools — bonus depreciation and cost segregation — allow investors to accelerate a portion of those deductions into earlier years, when the tax benefit is often most valuable.

Cost segregation is an engineering-based analysis that reclassifies components of a property from longer-lived categories into shorter-lived ones. Carpeting, lighting, specialized electrical systems, and certain site improvements may qualify for 5, 7, or 15-year depreciation schedules rather than the 27.5 or 39-year standard. By accelerating those deductions, the fund captures more of the tax benefit in the early years of ownership — when cash flow is being deployed and investors are most sensitive to their tax position.

Bonus depreciation allows qualified property to be fully deducted in the year it is placed in service, rather than over its useful life. For property placed in service after January 19, 2025, 100% bonus depreciation is available under current law. This means that a cost segregation study combined with bonus depreciation can produce a significant depreciation deduction in the year a property is acquired — not spread across decades.

Why scale matters here

The funds offered by Accountable Equity hold assets across a portfolio that includes four resort properties — Renault Winery Resort, Kent Island Resort, Bohemia Manor Farm, and LBI National Golf and Resort — with total asset value exceeding $125 million (company-reported). When cost segregation and bonus depreciation are applied across a portfolio of that scale, the resulting depreciation pools are meaningful. Investors in the funds receive their proportional share through the K-1. Consult your CPA for guidance on how your specific ownership percentage and tax situation interact with these deductions.

Passive Activity Rules: What You Need to Know Before You Invest

The IRS distinguishes between active and passive income. Passive losses — including the depreciation deductions from a real estate syndication — can generally only offset passive income, not ordinary W-2 income. This is the rule most investors encounter when they first explore real estate’s tax advantages, and it creates a common misconception: that the depreciation benefit is unavailable to high-earning professionals who don’t qualify as real estate professionals.

That is not entirely accurate. Passive losses that cannot be used in the current year are suspended — they carry forward and become available when the fund generates passive income in future years, or when the underlying assets are eventually sold and gains are recognized. The deductions are not lost; they are deferred.

Real estate professional status is a separate designation that, if met, allows passive losses to offset ordinary income. Meeting this test requires significant involvement in real estate activities — it is not available to most W-2 investors. Whether you qualify depends on your specific situation and the hours you spend in qualifying real estate activities.

The rules governing passive activity losses are detailed and fact-specific. Before investing in any real estate syndication, consult a CPA who is familiar with real estate syndications and passive activity rules. This post explains the mechanics — how you apply them to your situation requires professional guidance.

Tax Treatment on Sale: Long-Term Capital Gains and Depreciation Recapture

When a fund sells an underlying property, investors typically recognize two types of taxable events: long-term capital gains on appreciation, and depreciation recapture on the deductions taken during the hold period.

Long-term capital gains are taxed at preferential rates — currently 0%, 15%, or 20% depending on income — compared to ordinary income tax rates that may exceed 37% for high earners. Because syndication funds typically hold properties for multi-year periods, qualifying for long-term treatment is common.

Depreciation recapture refers to the portion of gain that is attributable to depreciation deductions previously taken. This gain is taxed at a maximum rate of 25% under current law — higher than the long-term capital gains rate on appreciation, but still well below ordinary income rates for most investors in this category.

Some funds use 1031 exchanges to defer recognition of gain when properties are sold and proceeds are reinvested into qualifying replacement assets. Whether a specific fund utilizes this structure varies — it is a question to ask during due diligence on any fund you are evaluating.

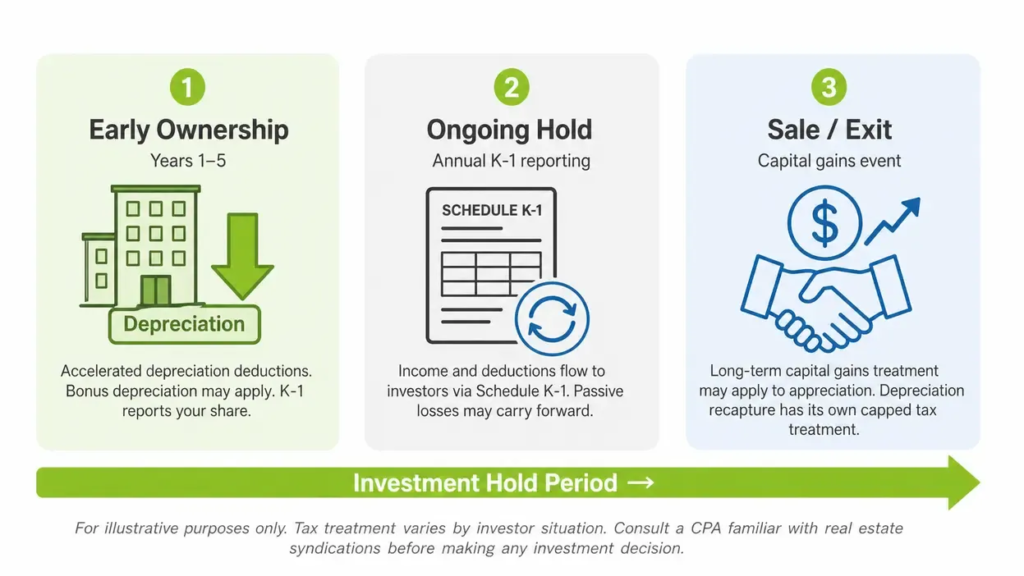

The tax picture over a full hold period

In a well-structured real estate syndication, the tax position often looks like this: early years feature elevated depreciation deductions that offset income; distributions during the hold period may be partially or wholly sheltered by those deductions; at sale, appreciation is taxed at preferential long-term rates and recaptured depreciation at the 25% rate. The net tax efficiency, compared to receiving the same total return through a brokerage account taxed at ordinary rates, can be substantial — but the specifics depend entirely on your income level, tax bracket, passive activity position, and the fund’s specific structure. Work with a CPA who understands real estate syndications before making any investment decision.

Real estate syndication tax treatment across a typical hold period. Consult your CPA for guidance specific to your situation.

Frequently Asked Questions

Do I receive a K-1 instead of a 1099 when I invest in a real estate syndication?

Yes. Investors in private real estate syndication funds structured as partnerships or LLCs taxed as partnerships receive a Schedule K-1 each year, not a 1099. The K-1 reports your share of the fund’s income, deductions, and other tax items. K-1s are typically issued after the calendar year ends — often later than standard brokerage 1099s — which may affect your tax filing timeline. Consult your CPA for the implications for your return.

Can I use depreciation losses from a syndication to offset my W-2 income?

Generally no — unless you qualify as a real estate professional under IRS rules. Depreciation deductions from a real estate syndication are typically classified as passive losses, which can only offset passive income. Unused passive losses carry forward to future years and become available when the fund generates passive income or when the underlying assets are sold. Your CPA can help you understand your specific passive activity position.

What is bonus depreciation and is it still available?

Bonus depreciation allows qualifying property to be fully deducted in the year it is placed in service, rather than over its standard useful life. For qualified property placed in service after January 19, 2025, 100% bonus depreciation is available under current law. When combined with a cost segregation study, this can produce a significant deduction in the year of acquisition. Consult your CPA for guidance on whether and how bonus depreciation applies to your situation.

What happens to my depreciation deductions when the fund sells a property?

When a property is sold, the IRS “recaptures” a portion of the gain attributable to prior depreciation deductions. Depreciation recapture is taxed at a maximum rate of 25% under current law — higher than the long-term capital gains rate on appreciation, but lower than ordinary income rates for most investors in the accredited investor income range. Your K-1 in the year of sale will detail these items. Consult a CPA familiar with real estate syndications before investing.

How does Accountable Equity approach tax structure in its funds?

The funds offered by Accountable Equity are structured as private placement vehicles under Regulation D Rule 506(c), available exclusively to verified accredited investors. The funds pass through tax items — including depreciation deductions — to investors via Schedule K-1. Questions about specific fund tax structures, cost segregation practices, or bonus depreciation application should be directed to Accountable Equity’s investor relations team and reviewed with your CPA and a securities attorney before any investment decision.

The Bottom Line

Real estate syndication offers a tax treatment that most accredited investors — particularly those who built their wealth in public markets — have never had access to. Depreciation, bonus depreciation, cost segregation, and K-1 pass-through treatment are not workarounds or loopholes. They are the direct result of owning an interest in a tangible asset through a properly structured vehicle.

The key phrase is “properly structured.” Not every real estate syndication is built the same way, and the tax benefits described here depend on the fund’s legal structure, the assets it holds, how cost segregation studies are conducted, and how the GP manages depreciation pools. Understanding these mechanics before you invest — and reviewing them with a CPA who is familiar with real estate syndications — is the difference between capturing these benefits and missing them entirely.

If you’re exploring real estate syndication as an investment category, learn more about how real estate syndication works and what verified accredited investors can access at Accountable Equity.