Vineyard National Golf Club at Renault Winery Resort, New Jersey — owned by Accountable Equity and operated by Vivamee Hospitality, both led by Josh McCallen. The structure visible behind the green is Louie’s Lounge, one of more than 20 event spaces on the property, operating year-round as a bar and gathering venue for golfers, event guests, and winter visitors watching the resort’s ice skating. Destination hospitality assets like Renault generate revenue across golf operations, resort accommodations, food and beverage, weddings and corporate events, and seasonal programming. Investment opportunities in assets like this are available exclusively to accredited investors.

A NOTE FOR READERS

This content is intended for informational and educational purposes only. Nothing here constitutes financial, legal, tax, or investment advice. Real estate syndication investments involve risk, including the potential loss of principal. Investors should complete their own due diligence and consult qualified professionals before making any investment decision.

Real estate syndication is not without risk. Any sponsor who tells you otherwise is not being straight with you, and that alone should tell you something about how they operate.

The honest answer to whether real estate syndication is safe is this: it depends on the quality of the sponsor, the structure of the deal, the underlying asset, and the fit between the investment and your financial situation. Syndications are private investments — they are illiquid, they are not FDIC-insured, and they carry real downside risk. Investors who understand that going in are in a much better position than those who discover it after the fact.

This guide explains the actual risks involved in real estate syndications, what causes most syndication failures, and what factors distinguish a well-structured deal from a poorly managed one. It also addresses what accredited investors should be asking before they commit capital to any private offering.

What You Will Find in This Guide

- The risks you may already be carrying in stocks and a 401(k)

- The real risks of real estate syndication — explained plainly

- What causes most syndication failures

- How deal structure affects risk

- The role of the sponsor in managing risk

- How to evaluate whether a syndication is appropriate for you

- Frequently asked questions

The Risks You May Already Be Carrying

Before examining the risks in real estate syndication, it is worth examining the risks most accredited investors are already carrying — often without having evaluated them as carefully as they are about to evaluate this one.

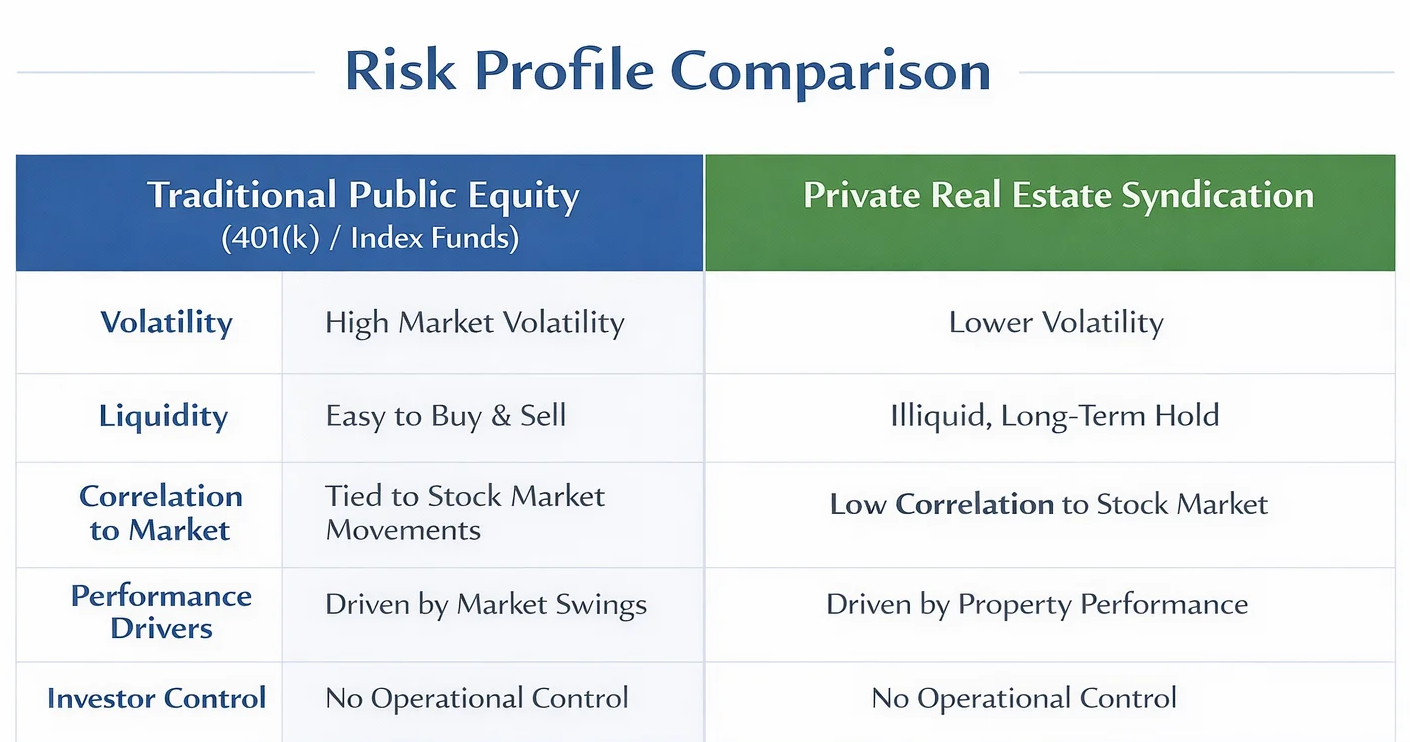

For investors whose primary financial exposure is stocks, index funds, and a 401(k), the risk profile of that portfolio is often described as familiar rather than genuinely safe. Familiarity and safety are not the same thing. The risks embedded in a conventional public equity portfolio are real — they are simply risks that most investors have normalized because they have always been there.

Market Volatility You Cannot Influence

Public stock markets experience significant drawdowns with regularity. The S&P 500 has experienced significant drawdowns on multiple occasions over the past two decades — including the dot-com collapse of 2001 to 2002, the financial crisis of 2008 to 2009, and the rate-driven correction of 2022, among others. During those periods, a portfolio concentrated in index funds declined in lockstep, regardless of the underlying quality of the businesses held. The investor had no ability to influence the outcome and no operational reality they could point to as a floor — just market sentiment and macro forces outside any individual’s control.

The volatility is visible and marked to market daily. That transparency can feel like safety — you always know what your portfolio is worth. But knowing the price and having control over the outcome are different things. A 401(k) that lost 35% of its value in 2008 did not become safer because the investor could watch the decline unfold in real time.

Concentration in a Single Market Cycle

A portfolio of domestic index funds and a 401(k) invested primarily in equities has correlation risk that is rarely named as such. When public equity markets decline, virtually all of the assets in that portfolio decline together — large cap, small cap, growth, value, and international tend to move in the same direction during periods of genuine market stress. Diversification across stock categories provides limited protection when the category itself — public equities — is the source of the stress.

This is the risk that leads sophisticated investors toward allocations in asset classes whose returns are driven by different underlying factors. Private real estate returns are tied to the operating performance of a specific asset — occupancy, revenue, and expense management — rather than to public market sentiment. That does not make private real estate risk-free, but it does mean the performance drivers are different, which is the basis for genuine diversification.

Sequence of Returns Risk

For investors approaching or in retirement, there is a risk specific to sequencing that is largely invisible until it is too late to address it. If a market decline occurs in the early years of retirement — when distributions are being taken from the portfolio — the portfolio may not recover to its prior value even if the market eventually recovers. The combination of withdrawals and declining asset values creates a compounding problem that is mathematically different from experiencing the same decline during the accumulation phase.

A portfolio with a meaningful allocation to private real estate — generating income from operating assets independent of public market pricing — provides a different kind of cushion during public equity drawdowns, not because private real estate is risk-free, but because its income and valuation are driven by different variables.

The Risk of Familiarity

There is a subtler risk worth naming: the risk of assuming that familiar investments are safe investments. Most investors never formally evaluated the risk profile of their 401(k) allocation — they accepted the default options their plan offered, set a contribution percentage, and periodically checked the balance. That approach has worked reasonably well during extended bull markets. It does not mean the portfolio is well-suited to the investor’s actual risk tolerance, time horizon, or income needs.

The point of this comparison is not to suggest that a 401(k) is the wrong vehicle — for most people, it is an important one. The point is to establish a level playing field for the risk conversation. Real estate syndication carries risks. So does a portfolio concentrated in equity index funds. The question is which risks you understand, which you are willing to accept, and how both fit into a portfolio genuinely designed for your situation.

Public equity and private real estate syndication carry fundamentally different risk profiles — not simply different levels of risk. The most important distinction for investors with significant stock market exposure is correlation: a 401(k) concentrated in index funds declines when markets decline, regardless of how the underlying businesses perform. Private real estate syndication returns are driven by property-level operations — occupancy, revenue, and management quality — which respond to different forces. Understanding both risk profiles is the foundation of genuine portfolio diversification. Consult a qualified financial advisor to evaluate how each category fits your specific situation.

The most useful way to evaluate any investment is not to ask whether it carries risk — all investments do — but to ask: What specifically are the risks? How do they interact with the rest of my portfolio? And which risks am I equipped to evaluate, manage, and absorb if they materialize? Those questions apply equally to a real estate syndication and to a target-date fund in a 401(k).

The Real Risks of Real Estate Syndication

Real estate syndications are private investment vehicles. Unlike publicly traded REITs or mutual funds, they do not trade on exchanges, they are not subject to the same disclosure requirements as registered public offerings, and they do not come with any form of government-backed protection. That regulatory structure is why access is limited to accredited investors — Regulation D’s exemption from SEC registration requirements is available only when the issuer has a reasonable basis to believe that investors have the financial means and experience to evaluate and absorb the risks of unregistered private offerings.

The risks that matter most fall into several categories.

Illiquidity

This is the most fundamental characteristic of private real estate investments, and it catches investors off-guard more often than any other factor. When you invest in a real estate syndication, your capital is committed for a defined holding period — typically three to ten years depending on the asset type, deal structure, and strategy. You cannot sell your position on a secondary market the way you might sell a stock or an ETF. If your financial circumstances change and you need liquidity before the hold period ends, your options are severely limited.

This is not a flaw in the structure — it is a feature that allows the sponsor to manage the asset for long-term value creation without the pressure of short-term redemptions. But it is critical that investors evaluate their liquidity needs honestly before committing capital to any private offering. Syndication capital should come from funds you can genuinely afford to have illiquid for the duration of the investment.

Capital Loss Risk

Private real estate investments carry real downside risk, including the potential loss of some or all invested principal. This is not a legal disclaimer tacked on for formality — it reflects genuine economic reality. Real estate values can decline. Operating businesses within a real estate asset can underperform. Debt structures can create pressure during downturns. Market conditions can shift in ways that were not anticipated at acquisition.

A well-structured syndication with an experienced operator significantly reduces — but does not eliminate — the probability of capital loss. Investors should size their exposure to any single syndication as part of a broader alternative investment strategy, not as a primary portfolio position.

Return Uncertainty

Syndications are structured with target returns — preferred return thresholds, projected equity multiples, internal rate of return (IRR) projections — but these are projections, not guarantees. The actual returns investors receive depend on how the asset performs against the underwriting assumptions made at acquisition: occupancy rates, revenue projections, operating expense estimates, and the exit environment when the asset is sold.

Projections that look compelling at the time of investment may prove optimistic if market conditions change, if the asset underperforms operationally, or if the exit environment for that asset class deteriorates. Experienced investors evaluate sponsors on how disciplined their underwriting is — whether projected returns appear achievable or whether they reflect aggressive assumptions designed to win investor commitments.

Sponsor and Execution Risk

This is the risk that receives the least attention in general discussions of syndication investing, and arguably the one that matters most. In a real estate syndication, the limited partner (LP) investor has no day-to-day operational control over the asset. The general partner (GP) sponsor makes decisions — on property management, on capital expenditures, on refinancing, on the timing and structure of the exit. Those decisions directly affect investor outcomes.

A highly competent sponsor with demonstrated experience in the specific asset class, a track record of delivering on projections, and the operational depth to manage through challenges is the single most important variable in whether a syndication performs. A sponsor who is good at raising capital but lacks genuine operating expertise is a materially higher-risk counterparty, regardless of how well the pitch deck is designed.

What Causes Most Syndication Failures

Most underperforming or failed syndications trace back to one or more of the following causes:

- Overleveraged deal structures where debt service becomes untenable when revenue underperforms or interest rates rise

- Sponsors who lack operational experience in the specific asset class and cannot manage through challenges that experienced operators would navigate

- Aggressive underwriting assumptions — occupancy rates, revenue growth, exit cap rates — that do not materialize in practice

- Misalignment of interests between the sponsor and investors, where the sponsor earns fees regardless of investor returns

- Poor asset selection — acquiring properties in markets with weakening fundamentals, at prices that leave insufficient margin for error

The common thread in most of these causes is sponsor quality. A well-capitalized, operationally experienced sponsor with a conservative underwriting philosophy and aligned incentives will encounter the same market conditions as a less capable competitor — but will typically navigate them more effectively. Evaluating the sponsor is not a perfunctory step in due diligence. It is the most important step.

How Deal Structure Affects Risk

Beyond the sponsor, the structure of a syndication deal itself carries meaningful risk implications. Several structural elements deserve careful evaluation.

Leverage and Debt Structure

Real estate syndications typically use debt financing to acquire properties — this leverage amplifies returns in favorable conditions but also amplifies losses when conditions deteriorate. The loan-to-value (LTV) ratio at acquisition, the nature of the debt (fixed vs. variable rate, recourse vs. non-recourse), and the duration of the loan relative to the projected hold period all affect how much cushion exists if the asset underperforms.

Syndications that acquired assets at high leverage ratios with short-term floating-rate debt during the low-rate environment of 2020 to 2022 faced significant pressure as rates rose. Conservative sponsors underwrite with sensitivity to interest rate risk and structure debt conservatively relative to projected cash flows. Investors should ask to see the sensitivity analysis in the offering materials — how does the investment perform if revenues come in 10% or 20% below projection?

Revenue Concentration vs. Multiple Revenue Streams

Some real estate assets generate revenue from a single source — a multifamily property depends entirely on tenant rent. Others, particularly destination hospitality assets, generate revenue across multiple streams: room revenue, food and beverage, event and function income, membership fees, and recreational fees. When one revenue stream is disrupted, the others continue generating cash flow.

Multiple revenue streams do not eliminate risk, but they can reduce the volatility of cash flows relative to single-source assets. For investors evaluating destination hospitality or experiential real estate assets specifically, understanding the composition and reliability of each revenue stream — and whether any portion is contractually guaranteed — is a meaningful part of risk assessment.

Preferred Return Structure and Waterfall

In most syndications, limited partner investors receive a preferred return — a priority claim on cash flows before the general partner earns any carried interest. The preferred return creates a structural protection that means investor capital is prioritized in distributions. However, the preferred return is not a guarantee of that return being paid on any specific schedule — it is a priority on distributions when cash is available.

Understanding the waterfall structure — the sequence in which cash flows are allocated between investors and the sponsor — helps investors understand under what conditions they receive distributions and what conditions must be met before the sponsor begins earning profit participation. Well-structured waterfalls align the sponsor’s compensation with investor outcomes.

The Sponsor’s Role in Managing Risk

The sponsor is not simply the person who found the deal and raised the capital. In a well-run syndication, the sponsor is responsible for every aspect of the investment’s lifecycle: acquisition underwriting, debt structuring, operational management, investor communications, and ultimately the exit. Each of these stages carries execution risk, and the sponsor’s capability in each area directly affects investor outcomes.

One of the most important distinctions in evaluating sponsor risk is the difference between a sponsor who is primarily a capital raiser — who sources deals, raises capital, and delegates management to third parties with no structural alignment — and a sponsor group whose ownership and operations entities share leadership and accountability. In the latter structure, the people responsible for investor capital and the people running the asset day-to-day are answerable to the same principal. That alignment reduces the conflicts of interest that arise when ownership and operations are entirely separate.

When evaluating a sponsor, the questions that matter most include:

- What is the sponsor’s track record in this specific asset class — not real estate generally, but this category of asset?

- How many deals has the sponsor taken full cycle (acquired and exited), and how did actual returns compare to projected returns?

- Does the sponsor manage the asset directly, or does it rely on third-party management?

- What is the sponsor’s experience managing through economic downturns — and did they have assets in operation during a meaningful period of market stress?

- How does the sponsor communicate with investors during the hold period — and what happens when the news is not good?

WHY ALIGNED OWNERSHIP AND OPERATIONS MATTER

Accountable Equity owns the properties and raises investor capital. Vivamee Hospitality manages resort operations. Both entities are led by the same principal, Josh McCallen. That shared leadership creates a structural alignment that a pure capital raiser — one that delegates operations to an unrelated third-party manager — cannot replicate.

When an operational challenge arises — a revenue shortfall, a capital improvement decision, a refinancing need — the ownership and operations entities are answerable to the same person. That accountability structure reduces the conflicts of interest that arise when the entity responsible for investor capital and the entity running the asset have no shared obligation.

Taste 1864, the signature restaurant at Renault Winery Resort, New Jersey, during an investor event hosted by Accountable Equity. Renault Winery Resort is owned by Accountable Equity and operated by Vivamee Hospitality — both led by Josh McCallen. The resort functions as a fully integrated destination — dining, accommodations, golf, wine production, and event programming on a single campus. For accredited investors evaluating a syndication structure, the relationship between the ownership entity and the operations entity — and specifically whether they share accountability to the same principal — is a meaningful part of sponsor due diligence.

How to Evaluate Whether a Syndication Is Appropriate for You

The question of whether real estate syndication is safe for you specifically requires an honest evaluation of several factors that are personal to your financial situation, not just the quality of the deal being offered.

Your Liquidity Position

Capital committed to a real estate syndication is generally illiquid for the hold period. Before investing, evaluate whether the capital you are considering committing represents funds you genuinely will not need for at least the projected hold period — plus a buffer for life events you cannot fully anticipate. If there is a meaningful probability that you would need to access those funds before the investment exits, private real estate is not the right vehicle regardless of the opportunity.

Your Risk Tolerance and Portfolio Composition

Private real estate should be evaluated as part of your overall portfolio allocation, not in isolation. For most accredited investors new to alternatives, syndications represent a portion of their investable assets allocated to private markets — not a replacement for a diversified portfolio. The appropriate allocation to any single syndication, and to private real estate overall, depends on your total assets, your income stability, and your broader financial plan.

Concentration risk — having too much capital in a single asset, a single sponsor, or a single asset class — is a genuine risk even in high-quality syndications. Sophisticated investors diversify across sponsors, asset classes, and vintages rather than concentrating in any single opportunity.

Your Ability to Evaluate the Sponsor

Investing in a syndication with a sponsor you cannot meaningfully evaluate is a higher-risk proposition than it may appear. The inability to assess sponsor quality does not make the investment safer — it makes the risk invisible. Before investing with any sponsor, take the time to understand their track record, their operational model, how they have performed in prior deals, and how they communicate during the hold period. If you cannot get satisfactory answers to basic due diligence questions, that is information about the sponsor.

Frequently Asked Questions

Is real estate syndication safer than the stock market?

The more accurate frame is that they carry different types of risk, not simply different levels of risk. As discussed above, stock markets are liquid and marked to market daily — which provides transparency but not control. Real estate syndications are illiquid, valued periodically, and carry significant sponsor execution risk. The meaningful distinction for investors coming primarily from public markets is correlation: a 401(k) concentrated in public equities will decline when markets decline, regardless of how well the underlying businesses are performing. A private real estate investment generating income from a specific operating asset is not correlated to that same event. That non-correlation is the basis for diversification — not a claim that private real estate is inherently safer, but that it responds to different forces.

Can I lose all of my money in a real estate syndication?

In extreme scenarios, yes — a total loss of invested capital is possible in a real estate syndication. This would require the asset to fail catastrophically, debt to be recourse to the equity investors, and the sale proceeds to be insufficient to cover investor capital. Total loss is not a common outcome in well-underwritten syndications with conservative leverage and experienced sponsors, but it is not impossible. This is precisely why the accreditation framework exists — investors are expected to have both the sophistication to evaluate this risk and the financial resources to absorb potential losses without catastrophic impact on their overall financial position.

How do I know if a syndication sponsor is trustworthy?

Trustworthiness in a syndication sponsor is established through a combination of verifiable track record, operational transparency, and the quality of their investor communications — not through marketing materials. Verify the sponsor’s prior deals through independent means where possible: SEC EDGAR filings for prior Regulation D offerings, references from past investors, and direct conversations with the management team. A sponsor who has managed assets through a difficult period and communicated honestly with investors during that period has demonstrated something more meaningful than a good return in a favorable market environment.

What is the difference between risk in a single-asset syndication and a fund?

A single-asset syndication concentrates your capital in one property. If that property performs well, your returns reflect its performance directly. If it underperforms, there is no other asset in the structure to offset it. A fund structure diversifies across multiple properties or deals, which reduces concentration risk but also reduces the direct visibility you have into any individual investment. For investors new to private real estate, fund structures can provide a smoother introduction to the asset class. For more experienced investors, single-asset syndications offer the ability to underwrite specific opportunities with greater precision.

I have always invested in index funds and a 401(k). Is syndication a reasonable next step?

For accredited investors exploring alternatives for the first time, private real estate has historically been used as a portfolio diversifier by investors with stable income, adequate liquid reserves, and capital available for a multi-year commitment. Whether that profile fits your situation is a determination that requires consultation with a qualified financial advisor. The realistic path for most first-time alternative investors is to start by educating yourself on how these structures work — the GP/LP structure, how distributions are made, how the waterfall functions — before committing capital. The learning investment pays for itself in your ability to ask better questions and make better decisions.

The Bottom Line

Real estate syndication is not safe in the sense of being guaranteed or risk-free. It involves real risks — illiquidity, capital loss potential, return uncertainty, and significant dependence on sponsor quality. Those risks are manageable for investors who understand them, evaluate them honestly against their own financial situation, and select sponsors with the experience, operational depth, and alignment of interests to navigate the inevitable challenges that arise in any long-hold investment.

The question is not whether syndication is safe in absolute terms. The question is whether the risk profile of a well-structured syndication with a credible, experienced operator is appropriate for your specific situation — and whether the potential return justifies that risk compared to alternatives. That is a judgment that requires genuine due diligence on both the sponsor and your own financial position.

If you are exploring how to evaluate a real estate syndication sponsor, our investor resources section covers the specific questions to ask and the criteria that distinguish institutional-quality operators from capital raisers with a polished pitch.

UP NEXT IN THIS SERIES

Accredited Investor Requirements 2026: Income, Net Worth, and How to Qualify

You understand the risks of real estate syndication. The next question most investors ask is whether they actually qualify to participate. The 2026 accredited investor thresholds, how the income and net worth test work, and what accreditation unlocks — covered in detail.

Part of the Accountable Equity Investor Education Series.