Bohemia Manor Farm, Maryland — a waterfront winery, vineyard, and event estate owned by Accountable Equity and operated by Vivamee Hospitality. Investment opportunities in destination hospitality assets like this are available exclusively to accredited investors.

In 2026, accredited investor status is defined by rules set under SEC Rule 501 of Regulation D. The two most widely used qualification pathways are an individual income exceeding $200,000 in each of the past two years ($300,000 combined with a spouse or domestic partner), or a net worth exceeding $1 million excluding the primary residence. A third pathway — qualifying through certain professional credentials — has been available since the SEC expanded the definition in 2020.

Understanding these requirements matters because they determine who can participate in private investment offerings: real estate syndications, private equity funds, venture capital, and other alternative investments that are exempt from SEC registration and not available to the general public. If you are reading this to determine whether you qualify, this guide walks through each pathway in the detail that a simple summary typically omits.

A NOTE FOR READERS

This content is intended for informational and educational purposes only. Nothing here constitutes financial, legal, tax, or investment advice. The accredited investor qualification rules involve legal standards that the SEC has left partially undefined by design. Investors should consult a qualified securities attorney or CPA to confirm their status before relying on any self-assessment in connection with a specific offering.

What You Will Find in This Guide

The income test: thresholds, what counts, and what the rules leave open

- The net worth test: the primary residence exclusion explained in full

- The professional credential pathway: which licenses qualify

- How entities qualify — and what conditions must be met

- How verification actually works under 506(b) and 506(c)

- Common questions and edge cases

Why the Requirements Exist

The SEC created the accredited investor designation to identify individuals presumed to have the financial sophistication and resources to evaluate private investments and bear their risks without the protections that registered public offerings are required to provide. Private offerings are not subject to the same disclosure and registration requirements as public securities — the accreditation threshold is the framework the SEC uses to limit these offerings to investors considered capable of independent evaluation.

The thresholds have not been adjusted for inflation since they were established in 1982, which means the pool of qualifying investors has grown substantially over the decades. Today, a significant portion of high-income professionals, business owners, and executives qualify without realizing it. The SEC has periodically reviewed whether to update the thresholds, but as of 2026, the income and net worth figures remain unchanged from the original rule.

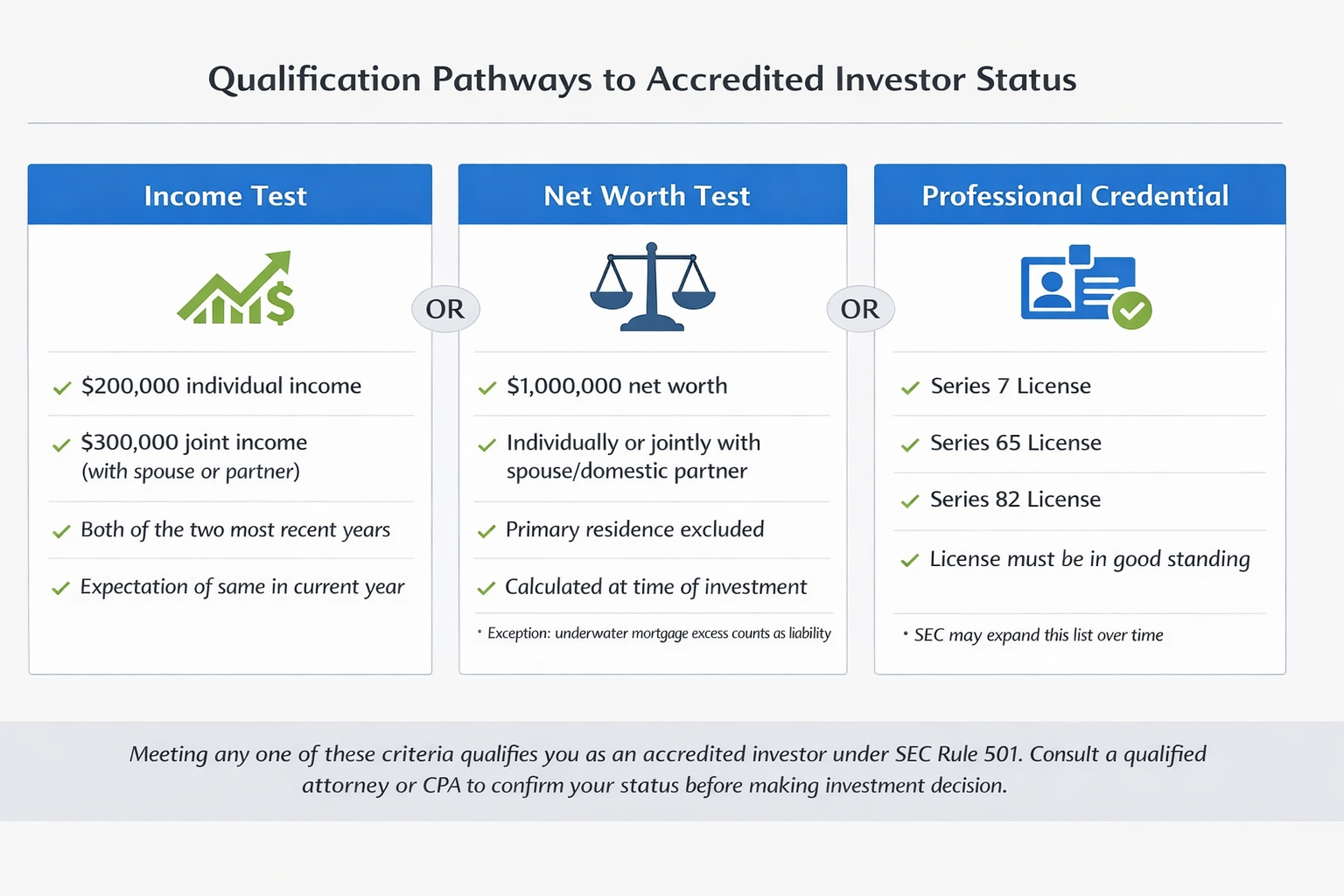

The Income Test

What the threshold requires: You must have earned more than $200,000 in individual income in each of the two most recent calendar years, with a reasonable expectation of earning the same in the current year. If qualifying jointly with a spouse or domestic partner, the combined income threshold is $300,000 for each of those same two years.

Both years must individually clear the threshold. One strong year preceded by a year below the threshold does not qualify. If your income crossed $200,000 for the first time last year, you will not meet the two-year requirement until the second year is complete.

The joint income pathway requires consistency in the filing relationship. The same spouse or domestic partner must be part of the joint calculation in both qualifying years.

What counts as income is not precisely defined in the rule. SEC Rule 501(a)(6) uses the term “income” without specifying whether it refers to gross income, adjusted gross income, or some other measure. In practice, income for accredited investor purposes generally encompasses wages, self-employment income, business distributions, investment income, capital gains, rental income, and most other forms of economic income. However, the specific methodology can vary depending on how a particular sponsor or their legal counsel applies the rule in connection with a specific offering.

This ambiguity has a practical implication: do not assume that a straightforward reading of your tax return will definitively answer the question. Your CPA is the appropriate resource for confirming how your income sources will be treated for purposes of accredited investor qualification in connection with any specific offering you are evaluating.

| INCOME TEST AT A GLANCE |

|---|

|

The Net Worth Test

What the threshold requires: A net worth exceeding $1,000,000, individually or jointly with a spouse or domestic partner, calculated at the time of the investment. The critical detail — and the one most commonly misunderstood — is that the value of your primary residence is excluded from the calculation on both sides.

The primary residence exclusion, explained. Before the Dodd-Frank Wall Street Reform Act of 2010, home equity could be counted toward the $1 million threshold. That changed with Dodd-Frank. Today, the fair market value of your primary residence does not count as an asset in the net worth calculation, and the mortgage debt on your primary residence does not count as a liability. The home and its associated debt are effectively removed from the equation entirely.

There is one exception to this exclusion. If the outstanding balance on your primary residence mortgage exceeds the fair market value of the home — meaning the property is underwater — the amount by which the mortgage exceeds the home’s value is counted as a liability. This prevents the exclusion from creating an artificial net worth boost in cases where the home carries negative equity.

What does count toward net worth under this framework: investment accounts (brokerage, taxable portfolios), retirement accounts (IRA, 401(k), SEP-IRA, pension values), cash and bank accounts, secondary real estate and investment properties, business ownership interests, vehicles, collectibles, and other tangible assets — minus all liabilities outside the primary residence mortgage.

A practical note: net worth is assessed at the time of investment, not at the end of the tax year or at the time of a prior filing. If your net worth has changed materially — in either direction — since your most recent financial assessment, the current figure governs.

| NET WORTH TEST AT A GLANCE |

|---|

|

The Professional Credential Pathway

In August 2020, the SEC amended Rule 501 to expand the accredited investor definition beyond purely financial thresholds. For the first time, individuals could qualify based on demonstrated financial sophistication rather than wealth alone.

Currently recognized credentials: The SEC specifically identified three licenses as qualifying pathways: the Series 7 (General Securities Representative License), the Series 65 (Investment Adviser Representative License), and the Series 82 (Private Securities Offerings Representative License). To qualify through this pathway, the license must be currently held in good standing — a lapsed or inactive license does not qualify.

Why this expansion matters: Many financial professionals — advisers, broker-dealer representatives, and others who work with securities daily — may qualify under this pathway even if their personal income or net worth does not clear the financial thresholds. The SEC’s position is that these individuals have the professional training to evaluate private investment risk, which serves the same protective goal the financial thresholds were designed to accomplish.

The SEC has indicated this list may expand. The 2020 amendments were framed as a starting point rather than a definitive list. The SEC noted it may designate additional credentials over time, but as of 2026, only the three licenses listed above have been formally recognized.

How Entities Qualify

Accredited investor status is not limited to individuals. Trusts, corporations, partnerships, LLCs, and other entities can qualify under separate provisions — but the conditions are specific and commonly misunderstood.

The $5 million entity threshold. An entity with total assets exceeding $5 million may qualify as an accredited investor, but only if two additional conditions are met: the entity must not have been formed for the specific purpose of acquiring the securities in question, and investment decisions must be directed by a person with sufficient knowledge and experience in financial and business matters to evaluate the merits and risks of the prospective investment.

The “not formed for the purpose of acquiring the securities” condition deserves attention. A newly formed entity created to pool capital from multiple investors for a specific offering would typically not qualify under this threshold. The entity must be an operating vehicle or investment structure with a broader purpose predating the offering. If there is any question about whether an entity qualifies, the sponsor’s counsel — not a self-assessment — is the appropriate resource.

Entities owned entirely by accredited investors. A separate provision covers entities in which all equity owners are independently accredited investors. If every owner meets the individual accredited investor criteria, the entity itself qualifies regardless of total asset size.

Certain institutional categories qualify automatically. Registered investment advisers, banks, insurance companies, registered investment companies, and certain other institutional categories qualify as accredited investors under the rule without meeting the asset threshold.

How Verification Actually Works

Understanding the requirements is one thing. Understanding how sponsors verify your status in practice is a distinct question — and the answer depends on which regulatory exemption the offering relies on.

506(b) Offerings. Under Rule 506(b), an issuer may not engage in general solicitation but may sell to an unlimited number of accredited investors. The issuer must have a reasonable basis to believe that investors qualify. In practice, this is typically satisfied through a questionnaire in the subscription documents where the investor affirms their qualification status. The issuer bears the reasonable-belief obligation — it is not a pure self-certification standard, but the documentation burden is relatively light when a sophisticated investor represents their status in writing.

506(c) Offerings. Under Rule 506(c), an issuer may advertise the offering publicly but must take reasonable steps to actively verify that all investors are accredited. Representation alone is not sufficient. Acceptable verification methods typically include reviewing tax returns or W-2s for the income test, obtaining a written confirmation from a CPA, attorney, or registered broker-dealer, or reviewing financial account statements for the net worth test. Third-party verification services that specialize in this process are also used.

An important note on verification timing. Some investors and sponsors refer to verification letters as having a set validity period, commonly cited as 90 days. This is an industry convention, not an SEC regulatory standard. The validity period for any verification documentation is governed by the specific offering’s requirements, not a fixed rule. Confirm documentation requirements directly with the sponsor when evaluating any specific offering.

The three pathways to accredited investor qualification under SEC Rule 501 as of 2026. Investors must satisfy only one pathway — not all three. Consult a qualified attorney or CPA to confirm how these thresholds apply to your specific situation.

Common Questions and Edge Cases

My income fluctuates. Does one low year disqualify me?

Yes, for that period. If either of the two most recent calendar years fell below the threshold, you do not currently qualify under the income test, regardless of longer-term income history. The two-year window resets. Investors with variable income — business owners, consultants, those with significant investment distributions — should track each calendar year independently. If your income is close to the threshold, your CPA should be involved in the analysis, because how certain income items are treated can affect the outcome.

Can a spouse’s income alone qualify us jointly if I have no income?

The joint income pathway requires combined income attributable to both spouses or domestic partners. A single spouse’s income does not by itself create a joint income pathway under Rule 501(a)(6). If your spouse independently meets the $200,000 individual threshold, some offerings allow participation as jointly-titled investors in certain structures, but the mechanics vary by offering. Confirm the approach with the sponsor and your legal counsel.

I have a net worth over $1 million primarily through investment accounts and a business interest. Does my home value affect this?

No. The primary residence exclusion only removes the home from both sides of the calculation. It does not affect the treatment of investment accounts, retirement accounts, or business ownership interests. If your net worth exceeds $1 million after removing your home and its mortgage, you qualify under the net worth test.

I hold a Series 7 license but my net worth is under $1 million. Do I qualify?

Yes, provided the license is currently in good standing. The professional credential pathway is a standalone qualification route — you do not need to meet the income or net worth thresholds if you hold a recognized license in active status.

Does my 401(k) count toward net worth?

Generally yes. Defined contribution retirement accounts (401(k), IRA, SEP-IRA) are typically counted as assets in the net worth calculation. Defined benefit pension plans require a present value calculation, which introduces complexity. Your CPA can help determine how your retirement assets should be reflected in your net worth assessment.

I am not yet accredited. Are there any syndication structures that allow non-accredited investor participation?

Yes, under certain conditions. Rule 506(b) of Regulation D permits issuers to include up to 35 non-accredited investors in a private offering, provided those investors meet a “sophisticated investor” standard. Under SEC Rule 506(b)(2)(ii), a sophisticated investor must have sufficient knowledge and experience in financial and business matters to be capable of evaluating the merits and risks of the prospective investment — either individually or through a purchaser representative.

Several important distinctions apply. First, the sophisticated investor determination is made by the issuer, not by the investor. A non-accredited investor cannot self-select into a 506(b) offering by asserting sophistication — the sponsor must independently evaluate whether the investor meets that standard and must be prepared to document that determination. Second, the 35 non-accredited investor limit applies across the entire offering, not per closing or per raise. Third, Rule 506(b) prohibits general solicitation entirely, which means an investor cannot discover a 506(b) offering through public advertising — they must have a pre-existing, substantive relationship with the sponsor or be introduced through a registered broker-dealer.

The practical result is that 506(b) non-accredited participation is narrow and sponsor-specific. It is not a broadly accessible pathway, and most sponsors operating under 506(b) do not routinely include non-accredited investors even where the rule permits it.

A NOTE ON ACCOUNTABLE EQUITY’S OFFERING STRUCTURE

Accountable Equity conducts its investment offerings exclusively under Rule 506(c) of Regulation D. Rule 506(c) permits general solicitation but requires that all investors be verified accredited investors. As a result, participation in Accountable Equity offerings requires meeting the accredited investor standards described in this post. This post describes 506(b) for general educational purposes only — it does not describe the structure of any current or future Accountable Equity offering.

If You Believe You Qualify

The next step is not to self-certify and move forward — it is to consult with your CPA or a qualified securities attorney to confirm your status in connection with any specific offering you are considering. The framework above is a guide to the rules; it is not a substitute for professional guidance on your individual situation.

If you are exploring how private real estate investments fit into a broader portfolio strategy, our investor resources section provides additional context on how real estate syndications work, what to look for in a sponsor, and how to approach due diligence as a first-time alternative investor. Understanding the accredited investor requirements is the first step. Understanding the investment category they unlock is the second.

UP NEXT IN THIS SERIES

What Are Alternative Investments? A Guide for High-Net-Worth Investors

Now that you understand the accredited investor requirements and the private investment opportunities they unlock, many investors ask a broader question: how do alternative investments as a category differ from traditional stocks and bonds, and what role do they play in a diversified portfolio?

Part of the Accountable Equity Investor Education Series.