The investment thesis for destination hospitality assets rests on three structural arguments: contractual revenue that protects against market cycles, operational complexity that creates a barrier to entry, and multiple simultaneous revenue streams that conventional real estate cannot replicate. Together, they produce a return profile unavailable in multifamily, self-storage, or any other asset class most accredited investors have previously accessed.

This is not a lifestyle pitch. “People love experiences” is a market observation, not an investment argument. A durable thesis has to survive a downturn, a management transition, and a decade of operating pressure. The 2025 US hotel performance data makes the case: overall occupancy fell 1.2% and RevPAR declined 0.3% — the first full-year declines since the pandemic — while luxury and upper-upscale properties posted RevPAR growth of +5.3% in the same period. That bifurcation is not cyclical noise. It is the thesis expressed in market data. This post explains each pillar and the conditions under which it holds.

Renault Winery Resort — a fund offered by Accountable Equity owns the asset; Vivamee Hospitality operates it. The property’s multiple revenue streams — events, vineyard and wine experiences, golf, dining, and lodging — illustrate the TRevPAR model in practice.

Pillar One: Contractual Revenue Provides Downside Protection

Events — primarily weddings and corporate functions — do not cancel the way leisure travel does. A bride does not postpone her wedding because the stock market drops. That structural characteristic produces something most real estate assets cannot: forward booking visibility. Weddings book 12 to 18 months in advance, and the US wedding services market reached an estimated $65–$100 billion in 2025, with event venues capturing the largest single share of guest budgets. A well-operated destination property enters its operating season with a significant portion of revenue already contracted — not forecast, but booked and deposited by guests whose planning horizon is measured in months, not days.

That is not how multifamily works. Rent rolls compress in a downturn. Leisure lodging demand contracts with consumer confidence. Contractual event revenue does neither — which is exactly what portfolio non-correlation is supposed to accomplish. Drive-to-destination properties within two to four hours of major population centers add a further structural advantage: they generate higher repeat visitation rates, lower distribution costs, and demand that is less exposed to fuel price shocks and air capacity constraints than fly-to resort markets. Guests who return because they love a place are not the same economic variable as transient travelers making a one-time booking decision.

The operational consequence is significant: a property entering its season with a contracted event calendar can staff, provision, and plan from confirmed demand rather than forecasted demand. That is a planning position most real estate operators never occupy.

Pillar Two: Operational Complexity Is the Barrier to Entry

The second pillar is counterintuitive. The complexity that drives most investors away from destination hospitality is the same reason the opportunity exists for those who can execute it.

Running a destination property at scale requires simultaneous management of rooms, food and beverage, event logistics across up to 13 concurrent weekend events, maintenance across hundreds of acres, and guest experience standards that drive repeat revenue. Miss one and the others suffer. Execute all consistently and you have built a competitive position that no new entrant can replicate quickly.

That is the moat. Most investors see the complexity as a liability. Sophisticated capital allocators see it as the entry barrier that protects their returns from commoditization.

The Vivamee Hospitality operating system — developed by Josh McCallen and Melanie McCallen, each with 25+ years of hospitality experience, including Josh’s tenure as President and Partner of ICONA Resorts (Inc. 5000 honoree three consecutive years; TripAdvisor’s #7 Best Hotel in the U.S.) — has been replicated across four distinct asset types since 2018. Both Accountable Equity and Vivamee Hospitality achieved dual Inc. 5000 recognition in 2025. Melanie McCallen’s role as Chief Experience Officer of Vivamee Hospitality is the capability that protects against the most common value-add failure in distressed hospitality: improving a property in the wrong direction. It is not replicable through a hired management company.

THE “COMPLEXITY AS BARRIER TO ENTRY” ARGUMENT IN ONE SENTENCE

The same characteristics that make destination hospitality difficult to operate are the same ones that protect investor returns when the right operator is executing the model. Complexity that deters competitors is complexity that earns a premium.

Why Conventional Metrics Miss the Thesis

Investors who approach destination hospitality with a conventional hotel underwriting framework will systematically undervalue the asset. The reason is the metric.

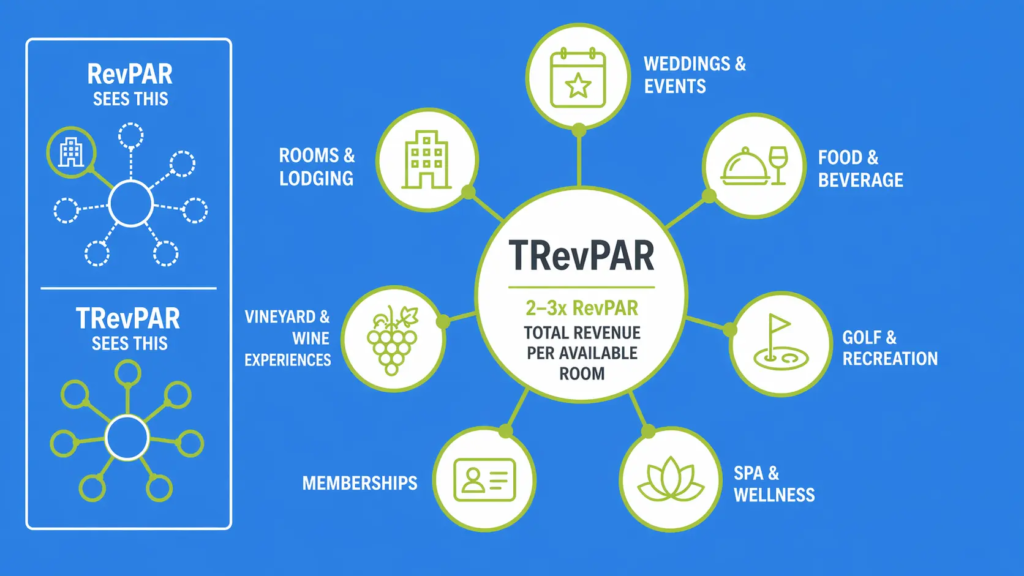

Average daily rate (ADR) measures the average room rate per occupied night. Revenue per available room (RevPAR) extends that to include occupancy. Both metrics capture only the rooms revenue line — which, in a multi-stream destination property, is one of several revenue channels running simultaneously.

Accountable Equity uses TRevPAR — total revenue per available room — as the correct evaluative metric for its portfolio. TRevPAR captures rooms, events, food and beverage, golf, memberships, vineyard and wine experiences, agri-tourism, and all other revenue channels in a single figure referenced to the room count. For a well-operated boutique destination resort, TRevPAR routinely runs two to three times higher than RevPAR alone. A property generating $180 in RevPAR may be producing $380 or more in TRevPAR. The $180 is what a RevPAR-focused underwriter sees. The $380 is what the business is actually worth — and what drives NOI, enterprise value, and long-term cash flow stability. An investor who benchmarks only on ADR or RevPAR will undervalue the asset and systematically misprice it relative to an investor reading the full revenue picture.

This distinction matters for due diligence. When evaluating any destination hospitality operator, ask for TRevPAR data — not just RevPAR. Ask how many revenue channels are active at the property, what the contractual versus discretionary revenue split looks like, and what forward booking visibility looks like at any given point in the year. An operator who cannot answer those questions in detail is not operating a multi-stream asset. They are operating a hotel.

Destination hospitality assets generate revenue across rooms, events, dining, golf, memberships, and agri-tourism simultaneously. This multi-stream model is what TRevPAR captures — and what conventional hotel metrics miss entirely.

Pillar Three: Tangible Scale Creates Returns Conventional Real Estate Cannot Replicate

The Vivamee portfolio spans 1,000+ acres, 2.5 miles of waterfront, and 320,000+ annual guests across winery resorts, a waterfront boutique property, a golf resort, and a working farm event venue. Those figures are operational scale proof points, not lifestyle metrics. At that volume, guest loyalty and repeat visitation compound into revenue trajectory that does not appear on a cap rate analysis.

The individual revenue streams each carry structural weight. US golf participation reached 29.1 million on-course players in 2025 — the eighth consecutive year of growth, approaching all-time records. A destination resort with golf capability monetizes that demand year-round, independent of room occupancy. Golf, events, spa, dining, and membership each contribute to TRevPAR in a way that compounds rather than simply sums: a guest who plays golf, dines twice on property, and books a spa treatment may generate three to four times the revenue of a room-only transient guest at the same ADR. Destination hospitality assets are also nearly impossible to replicate from scratch. Land in proximity to major metro areas is finite. Permits, historic designations, and established guest communities take years to build. Meanwhile, a $48 billion CMBS maturity wave hitting commoditized full-service hotels in 2025–2026 — with hotel CMBS delinquency surging and 40–45% of full-service hotel loans flagged as potentially troubled — is creating distressed acquisition opportunities in character-rich properties that operators with the right depth can reposition. Boutique capital market liquidity grew 55% post-pandemic versus only 3% for branded properties. That is the capital market confirming, in its own language, what the operating data shows.

Evaluating the Thesis: What to Verify Before You Invest

A thesis statement is not a due diligence substitute. For this thesis to hold in a specific investment, three things need to be verifiable.

First, confirm operator depth. Multi-revenue-stream execution requires a track record across multiple asset types and adversarial operating conditions. An operator who has only run a portfolio in favorable conditions has not been tested where the thesis matters most. Second, confirm contractual revenue with actual data — forward booking schedules, cancellation history, and the percentage of total revenue that is contractually committed at any point in the calendar. Projections are not enough. Third, evaluate platform trajectory. A family office or institutional allocator is not evaluating a single property — they are evaluating whether the operator is building a platform worth long-term allocation. The 25-resort-by-2035 growth target and dual 2025 Inc. 5000 recognition across both the capital formation and operating entities are the signals that matter here.

The most efficient due diligence tool for this asset class is a property visit during peak operations. Documents tell part of the story. Walking Renault Winery Resort on a peak summer event weekend — observing 13 concurrent events, the guest experience systems, and the operational team in motion — provides evidence that no private placement memorandum can convey.

Participation in Accountable Equity offerings is limited to verified accredited investors under Regulation D Rule 506(c). Accredited investors meet net worth thresholds of $1 million excluding primary residence, or income of $200,000 individually ($300,000 jointly) for the prior two years. Consult a securities attorney familiar with private placements before evaluating any specific offering.

Related reading: For context on how syndications work structurally, see “how real estate syndication works.” For a comparison of hospitality and multifamily as asset classes, see “hospitality real estate vs multifamily.” For the structural argument that vertical integration protects investor capital, see “why vertical integration matters when choosing a real estate sponsor.”

Frequently Asked Questions

What is the investment thesis for destination hospitality assets?

Three structural arguments: contractual revenue from events that does not cancel with the economic cycle, operational complexity that functions as a barrier to entry, and multiple simultaneous revenue streams that conventional hotel metrics systematically undercount. Together, they produce a return profile conventional real estate cannot replicate.

Why use TRevPAR instead of RevPAR or ADR for destination hospitality?

ADR and RevPAR capture only room revenue. A destination property generates revenue across events, dining, golf, memberships, vineyard and wine experiences, and other channels simultaneously. TRevPAR — total revenue per available room — is the only metric that reflects the full operating model. Investors benchmarking on RevPAR alone will undervalue the asset and misread its operating leverage.

How does contractual revenue protect investors in a downturn?

Weddings and corporate events booked 12 to 18 months out do not cancel when consumer confidence drops or the stock market falls. That structural disconnection from the economic cycle is the protective mechanism — confirmed revenue from guests whose commitment horizon is measured in months, not in daily sentiment shifts.

Is destination hospitality investing available to individual accredited investors?

Yes, through private placement funds structured under Regulation D Rule 506(c), available exclusively to verified accredited investors. This content is educational and does not constitute an offer to invest. Consult a securities attorney familiar with private placements before evaluating any specific offering.

The Thesis in Summary

The investment thesis for destination hospitality assets is not complicated, but it requires the right operator to hold. Contractual revenue provides the downside floor. Operational complexity provides the barrier that keeps under-capitalized and under-experienced operators out. Multiple revenue streams provide the growth ceiling. All three work together — or none of them work at all.

For sophisticated investors building portfolios designed to perform across full economic cycles, destination hospitality belongs in the conversation. Not as a lifestyle allocation, not as a speculative bet on travel trends, but as a structurally differentiated asset category with return drivers that are genuinely non-correlated to what the rest of a typical accredited investor’s portfolio is doing.

If you are evaluating this thesis at the operator level, the right next step is to visit the asset during peak operations. Documents, decks, and financial models tell part of the story. A property visit during a peak event weekend — where you can see the operation, the scale, and the guest experience firsthand — tells the rest. That visit is not a sales event. It is the most efficient due diligence tool available for an asset class where operational execution is the primary investment driver.