Real estate investors in private syndications are paid through distributions — periodic cash payments funded by asset income. Most funds also structure a preferred return for limited partners: a minimum threshold investors receive before the sponsor shares in profits. Understanding both mechanics, and how they connect to the waterfall that governs the full distribution sequence, is how you evaluate a fund correctly rather than be surprised by it after committing capital.

Private real estate syndication investments of the type described in this post are available only to independently verified accredited investors as defined by applicable securities laws.

Understanding the distribution waterfall is the foundation for evaluating any private real estate fund. The exact terms — including split percentages and preferred return mechanics — are defined in each fund’s offering documents.

What Is a Distribution in Real Estate Investing?

A distribution is a payment made to investors from fund cash flow. Whether a distribution is made in any given period — and in what amount — depends on the terms of the offering documents, not simply on whether the underlying asset generated income. A property may produce operating income and still retain that cash for reserves, capital improvements, debt covenants, or other purposes specified in the PPM. Investors should understand the distribution policy for any fund they evaluate before committing capital.

Distribution schedules vary by fund. Some target monthly, quarterly, or annual distributions. The cadence should reflect the underlying asset’s income cycle — a hospitality portfolio that generates revenue seasonally, for example, may structure distributions on an annual basis to account for the full operating year. Ask how any fund you evaluate structures its distribution policy, what conditions trigger a distribution, and what circumstances can delay or reduce one.

The key question before investing is not just how much you may be paid, but what drives that payment — and under what conditions. Distributions funded by operating income are structurally different from distributions funded by reserves or new investor capital. Understanding the source matters as much as the amount.

What Is a Preferred Return?

A preferred return — often called a “pref” — is a structural priority defined in the offering documents. It establishes a minimum threshold that limited partners are entitled to receive, per the PPM, before the general partner participates in profits above the hurdle. If a fund targets an 8% preferred return and you invest $100,000, the structure allocates the first $8,000 of any distributable profits to LPs before the GP takes carried interest. Whether that amount is actually distributed — and when — depends on fund performance and the specific terms of the offering.

The preferred return is not a guarantee. It is a structural priority — an alignment mechanism that puts LP capital first in the distribution sequence.

Two terms govern its mechanics and are worth understanding before signing anything. Cumulative vs. non-cumulative: a cumulative pref means unpaid amounts accrue and must be satisfied before the GP profits in future periods; non-cumulative means shortfalls do not carry forward. Compounding vs. simple: a compounding pref accrues on both original principal and any unpaid balance. Both distinctions affect investor economics meaningfully over a multi-year hold — and both are defined in the PPM, not the marketing summary.

Always read the Private Placement Memorandum carefully for the exact language governing the preferred return structure. The summary deck and the offering documents may not use identical terms — the PPM controls.

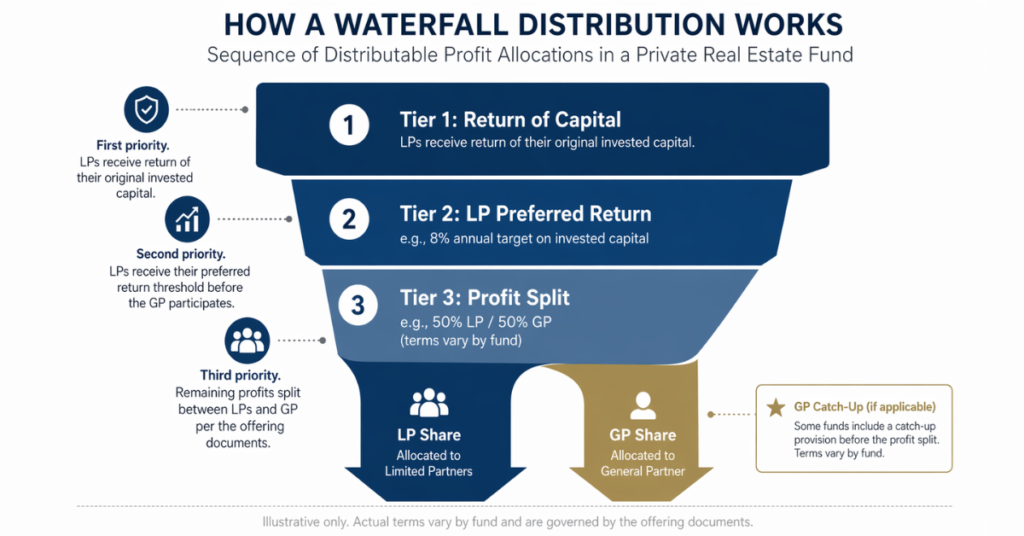

How Does the Waterfall Distribution Work?

The waterfall is the sequence in which profits are distributed between LPs and the GP. Most private real estate syndications use a two-tier or three-tier waterfall. Here is how a common two-tier structure works:

- Tier 1 — Return of Capital: Per the offering documents, LPs are entitled to return of their original invested capital before the GP participates in any profits. This typically occurs at sale or refinance, not during the operating period.

- Tier 2 — Preferred Return: LPs are entitled to their preferred return on invested capital before the GP participates above the hurdle. The specific mechanics — whether it accrues, compounds, and how shortfalls are treated — are defined in the PPM.

- Tier 3 — Profit Split: Any remaining profits are split between LPs and the GP per the offering terms. A common structure is 70% to LPs and 30% to the GP, though structures vary widely. Some agreements include a GP catch-up provision. Always confirm the exact split in the offering documents.

Why this matters for evaluation

A fund that offers a high stated return but structures carried interest to flow before LPs have received their full preferred return is not aligned with you. The waterfall tells you whose interests are prioritized and in what order. Compare waterfall terms across funds — not just headline return figures.

Cash-on-Cash Return vs. Total Return: Understanding the Difference

Two return figures appear in nearly every private real estate offering: cash-on-cash return and total return (often expressed as an equity multiple or an IRR). They measure different things, and confusing them leads to inaccurate underwriting.

Cash-on-cash return measures annual income distributions relative to invested capital. In a hypothetical example: invest $100,000, receive $8,000 in distributions for the year, and the cash-on-cash return for that period is 8%. This metric reflects what the fund actually distributed relative to your capital — not what it projected.

Total return (equity multiple or IRR) accounts for distributions during the hold period plus profit at sale. A fund with modest annual distributions but strong appreciation at exit may produce a strong total return despite a lower cash-on-cash figure.

The right question is not which metric is larger — it is what drives the projected return, and whether the asset’s operating model can support that projection. A hospitality asset with contracted event revenue booked 12 to 18 months in advance provides more verifiable cash flow visibility than one dependent on a single income source.

Timelines: When Do Real Estate Investors Actually Get Paid?

Private real estate investments are illiquid — and that is the mechanism through which the return opportunity is structured to exist. Investors who accept a hold period and forgo public market liquidity are intended to be compensated for that constraint through the preferred return priority, the waterfall alignment, and the return structure of the fund. Whether the actual return justifies that tradeoff depends entirely on fund performance.

A $100,000 investment at an 8% annual targeted preferred return in a five-year hold fund is a longer-term capital commitment, not a liquid savings product. Due diligence should focus on whether the asset, the operator, and the fund structure can realistically support the distributions projected in the offering materials — and what happens if they cannot.

A typical private real estate syndication follows this general timeline — though the specific offering documents always govern:

- Capital is deployed at closing and moves from your account to the fund.

- Distributions, if and when made, depend on fund performance and the terms of the PPM — not solely on whether the asset generated income. A stabilized asset may begin distributions within the first year; a value-add scenario may defer distributions until repositioning is complete. Either way, the offering documents will specify the conditions under which distributions are made.

- At sale or refinance, proceeds are distributed to investors per the waterfall defined in the PPM. The timing and amount depend on exit conditions, debt obligations, reserves, and other factors. Most private real estate funds target hold periods of three to seven years, but hold periods can extend beyond projections.

Frequently Asked Questions

How are real estate investors paid in a syndication?

Investors in real estate syndications may receive distributions — cash payments made from fund cash flow per the terms of the offering documents. Whether a distribution is made, in what amount, and on what schedule is governed by the PPM, not automatically triggered by asset income. Most funds also structure a preferred return for limited partners: a minimum threshold LPs are entitled to receive before the sponsor participates in profits above the hurdle.

What is a preferred return and how does it work?

A preferred return is a structural priority defined in the offering documents. It establishes a minimum threshold that limited partners are entitled to receive before the general partner participates in profits above the hurdle. If a fund targets an 8% preferred return on a $100,000 investment, the first $8,000 of any distributable profits is allocated to LPs before the GP takes carried interest. It is not a guarantee of payment — whether and when it is paid depends on fund performance and the PPM terms.

What is a waterfall distribution in real estate?

A waterfall is the sequence in which profits are distributed between limited partners and the general partner, as defined in the offering documents. A common structure allocates distributable profits first to return of LP capital, then to the LP preferred return, then splits remaining profits between LPs and the GP. The exact terms — including the split percentage, any GP catch-up, and what triggers each tier — vary by fund and are governed by the PPM.

Is the preferred return guaranteed?

No. A preferred return is a structural priority — a distribution sequencing commitment — not a performance guarantee. If the fund does not generate sufficient income to cover the preferred return, investors may not receive the full amount in a given period. Always review the specific terms in the Private Placement Memorandum.

The Bottom Line

Understanding how real estate investors are paid is not about memorizing terms. It is about knowing which questions to ask: Does the preferred return accrue if not fully paid? Where does the GP begin participating in profits? Is the distribution projection supported by an operating model you can verify?

The mechanics of preferred returns, waterfall distributions, and hold-period timelines are the tools that answer those questions. The sponsor who can walk you clearly through each of them has already told you something meaningful about how they think about alignment with investors.

Investors considering private real estate placements should review all offering documents carefully and consult qualified legal, financial, and tax advisors before making any investment decision.

📖 Up Next in This Series

What Is the Investment Thesis for Destination Hospitality Assets?

Now that you understand how private real estate investors are paid, the next logical question is what kind of asset best supports those mechanics. The follow-up post makes the case for why destination hospitality — with its contractual revenue, multiple income streams, and operational complexity as a competitive moat — produces a return profile that conventional real estate cannot replicate. Publishing Monday, April 27.